LA Newsletter

Note: You can find the charts & graphs for the Big Story at the end of the following section.

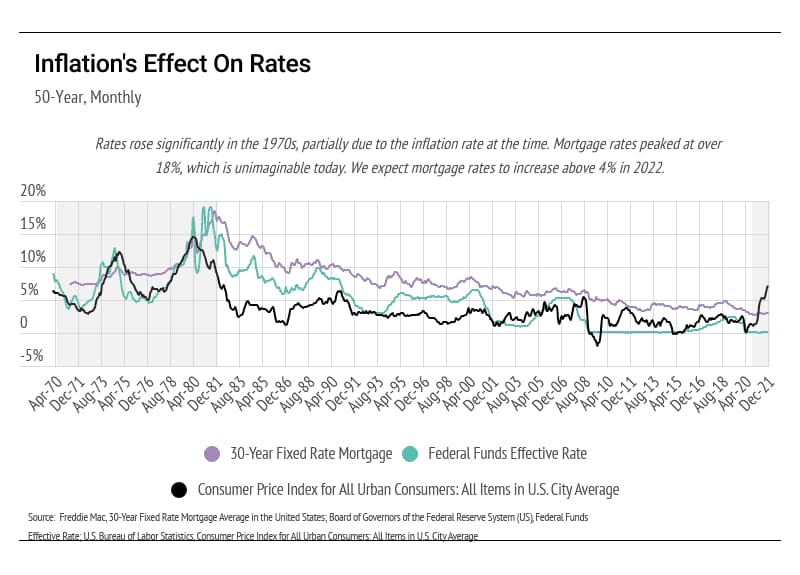

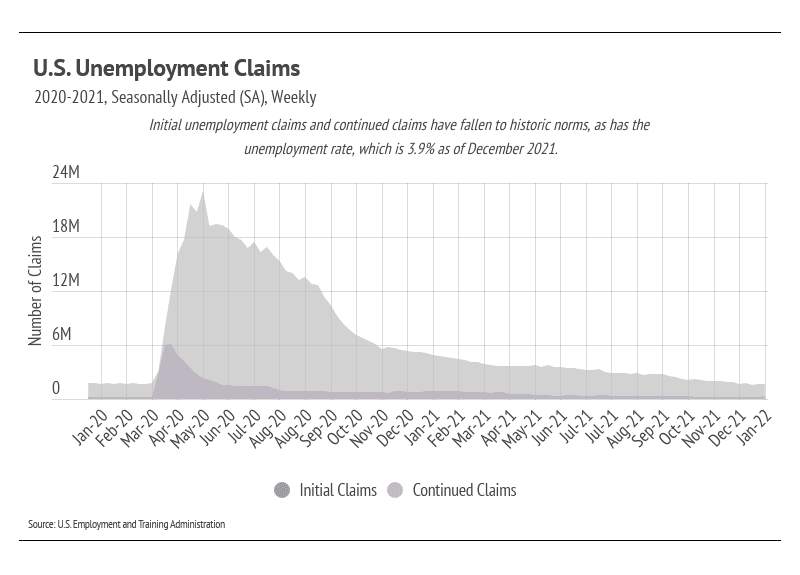

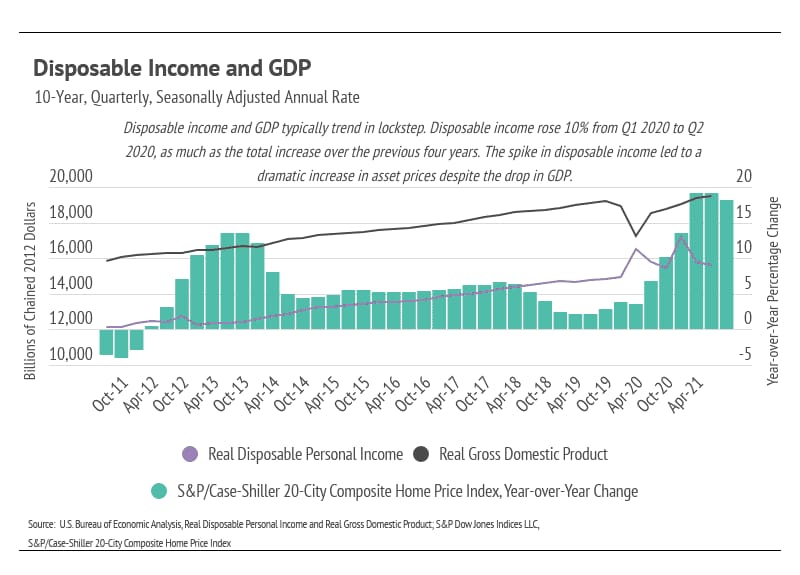

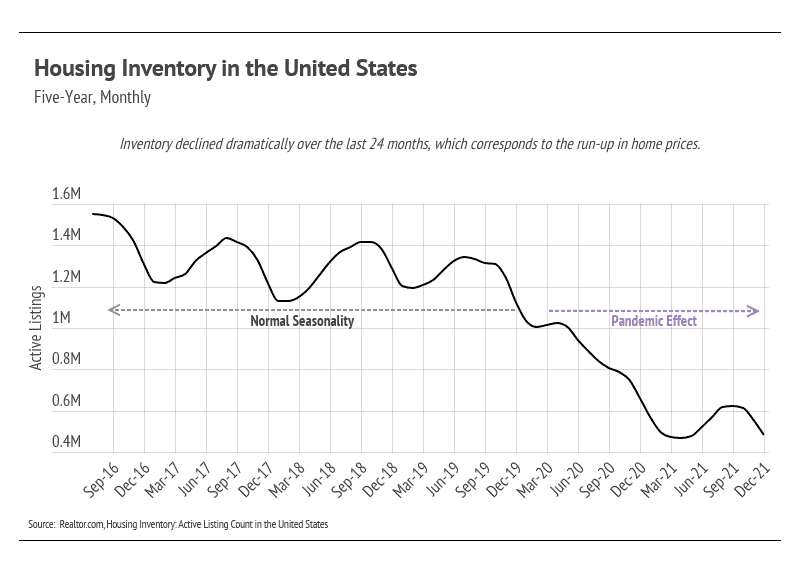

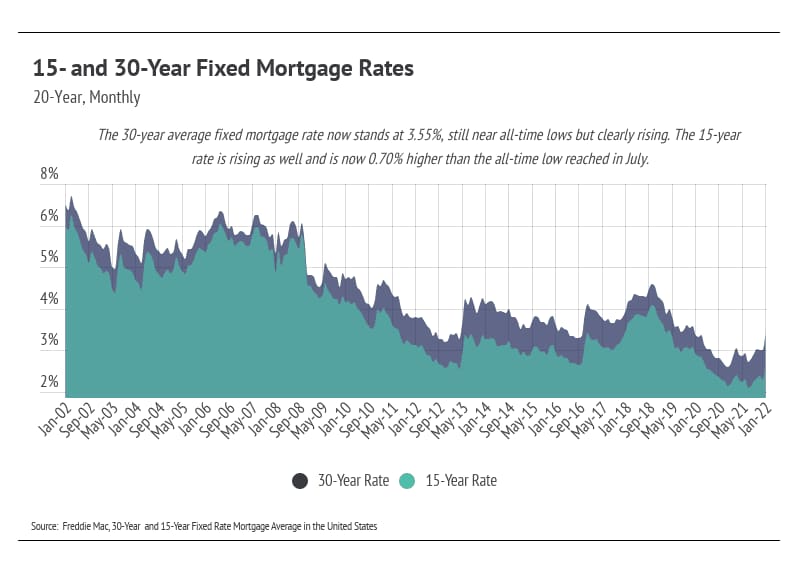

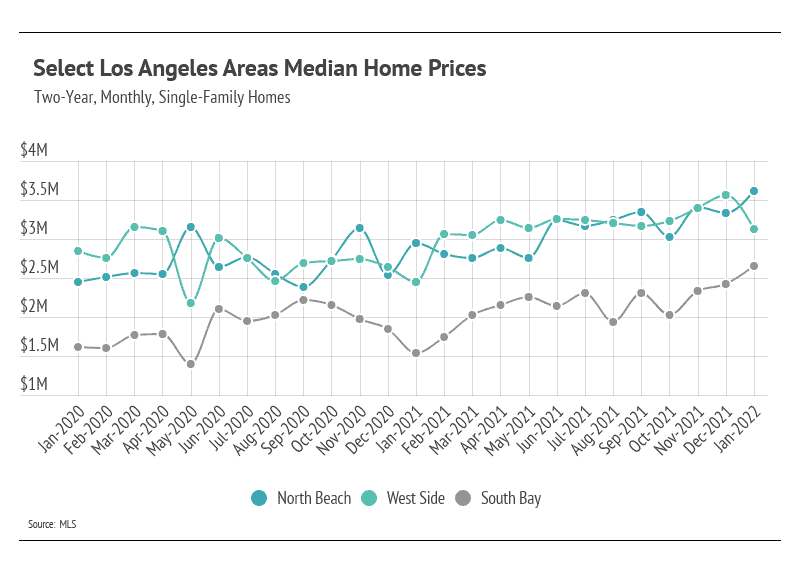

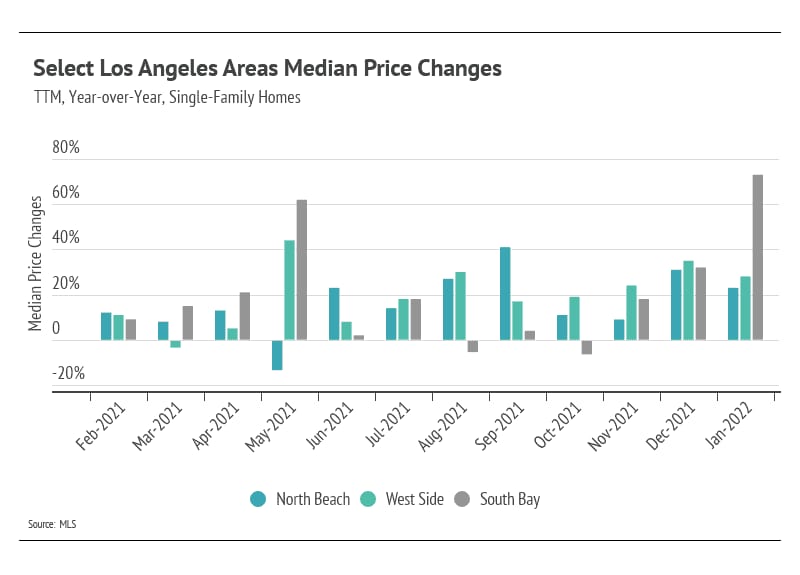

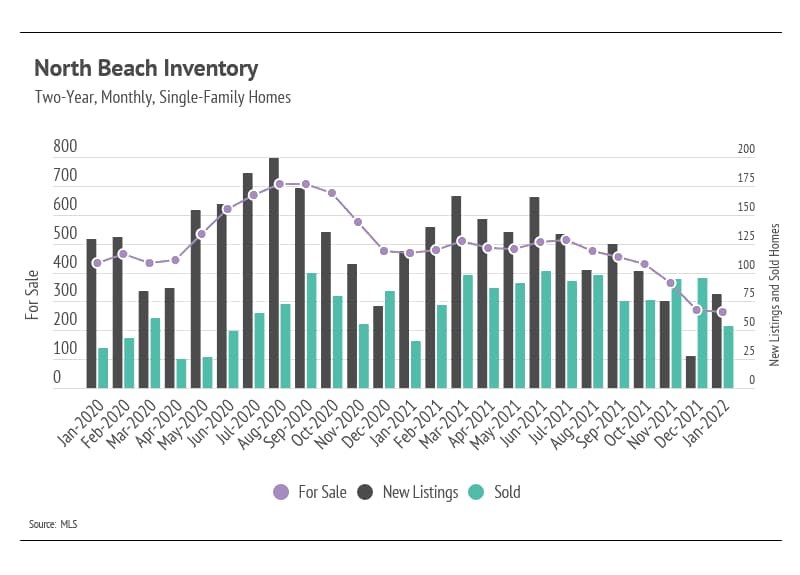

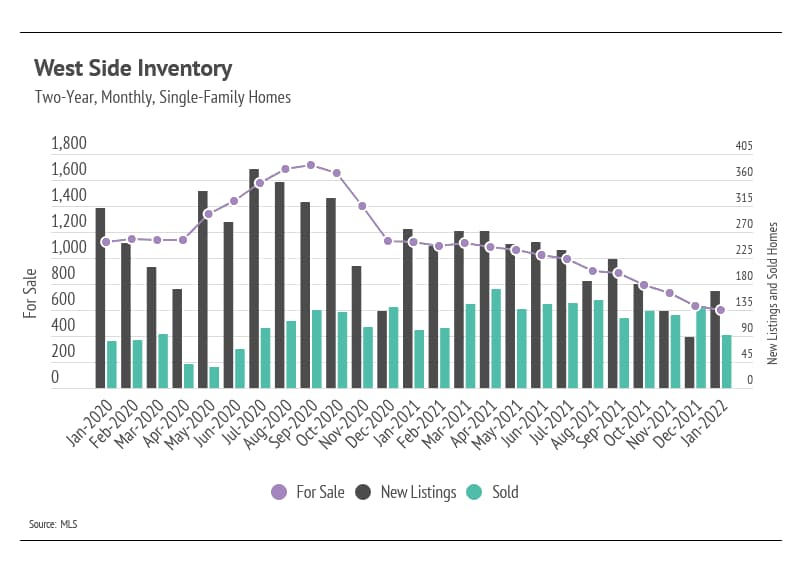

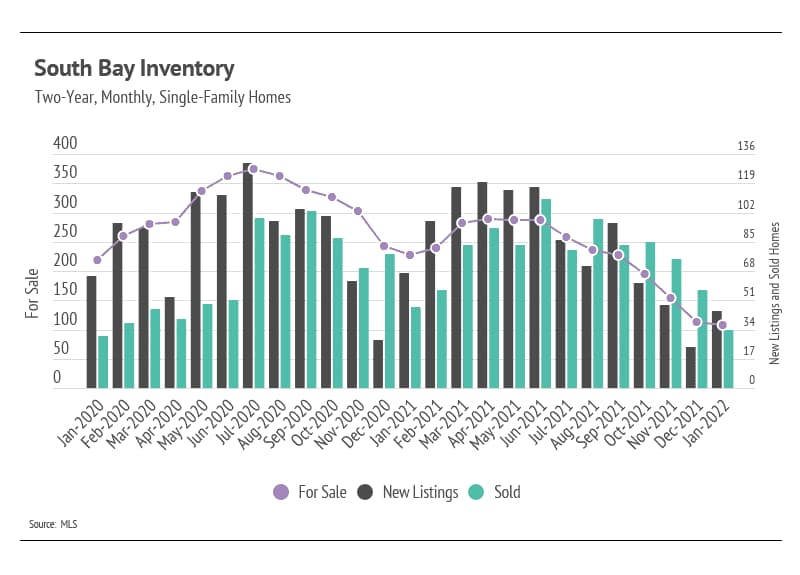

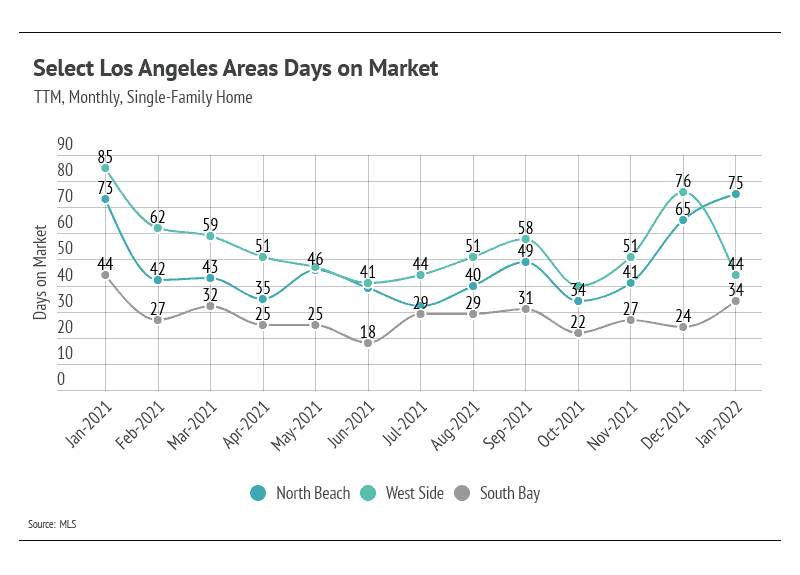

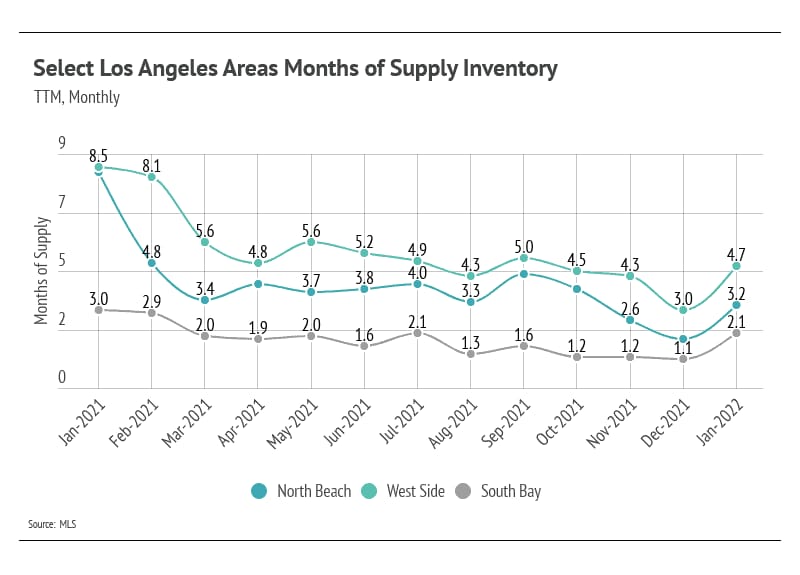

| On January 26, 2022, the Federal Reserve (the Fed) indicated that it would raise the federal funds rate as soon as March for the first time in over three years. The Fed adjusts the federal funds rate to influence broader interest rates, which directly affect the borrowing costs of banks. Generally, if bank borrowing costs are low, consumer borrowing costs will be low(er), and vice versa. The Fed uses interest rates in particular as a tool to meet its dual mandate of maximum employment and price stability. Employment and price stability are long-term indicators for home prices. We will start with the good news. Employment rebounded considerably from the highest spike in unemployment in modern history in spring 2020 to pre-pandemic levels by December 2021. As you might imagine, high unemployment rates for extended periods lead to less overall wealth: Fewer people buy homes, and more people experience foreclosures, thereby lowering home prices. Although unemployment seemed dire in 2020, employment is now on solid ground. If we view the current record-high 10.5 million job openings, along with the nearly 10 million new businesses created over the past two years, we get a better understanding of why unemployment dropped so significantly despite a record number of job openings. Simply put, people are working, and that is good for individual wealth and the larger economy. On to the kind-of-good, kind-of-bad news … rising mortgage rates could help curb inflation and create a more balanced housing market (although 2022 will surely be a sellers’ market), but it will make homes more expensive monthly, hitting first-time homebuyers the hardest. With the federal funds rate at 0% and inflation at a near-40-year high, rate hikes are expected to combat inflation. Essentially, when the cost to borrow increases, fewer people want to borrow, leading to less consumer spending (less demand), which lowers prices. We can look to the last inflationary period, the 1970s, as a loose guide. Inflation today is likely to be much more transitory than it was in the 1970s, but we can still expect a rise in mortgage rates like we saw then. Luckily, however, we will certainly not reach the 18+% mortgage rate that we saw in the early 1980s. As it was then, the Fed is obligated to do something now. While we wish that we could always be in periods of high employment, low inflation, and low interest rates, as we experienced for nearly a decade before the pandemic, we must recognize the atypical nature of that period. As we enter this new chapter of rising mortgage rates, we don’t expect home prices to change significantly, if at all, because supply is still such a driving factor. In December 2021, there were 57% fewer homes on the market than in December 2019. The low supply means that demand can decline without affecting prices. Does it matter if 10 offers drop to five? Probably not, and it might even create a better market. Sellers tend to become buyers, so unless you’re a first-time homebuyer, you’ll likely experience both sides of the market. Because sellers are often selling one home and buying another, it’s essential that sellers work with the right agent to ensure the transition goes smoothly. We don’t expect price appreciation to see the record gains we experienced over the past two years, but we do expect home prices to increase. Another factor at play over the past two years was a sharp increase in disposable income, which has now normalized. People had more money to spend over the past two years, and we saw that throughout markets: The housing market, the stock market, cryptos, art, jewelry, etc. all reached record high prices. As disposable income has dropped to a more normal level, we can expect assets to appreciate at a more normal pace. |

Stay up to date on the latest real estate trends.

Blog

Supporting Our Community: Resources and Ways to Help Los Angeles Recover from Wildfires

Quick Take: The Fed almost certainly will raise rates in March in an effort to combat inflation. Historically low supply is protecting the record-setting home prices o… Read more

If you’re planning to buy a home this year, saving for a down payment is one of the most important steps in the process. One of the best ways to jumpstart your savings… Read more

Over the past year, we’ve had plenty of opportunities to reflect on what we consider most important in our lives. The place we call home is one of the biggest things m… Read more

Over the past two years, the substantial imbalance of low housing supply and high buyer demand pushed home sales and buyer competition to new heights. But this year, t… Read more

With higher mortgage rates, you might be wondering if now’s the best time to buy a home. While the financial aspects are important to consider, there are also powerful… Read more

As the market has cooled this year, some of the intensity buyers faced during the peak frenzy of the pandemic has cooled too. Here are just a few trends that may benef… Read more

You’ve got questions and we can’t wait to answer them.